India’s Carbon Credit Trading Scheme (CCTS) has transitioned from policy to balance sheet reality. The Ministry of Environment, Forest and Climate Change (MoEFCC) has notified Greenhouse Gas (GHG) emissions intensity targets, acting on recommendations from the Bureau of Energy Efficiency (BEE), on October 08, 2025. These targets are applicable to the identified Obligated Entities across cement, aluminium, chlor-alkali, and pulp and paper sectors. Sectors such as Iron & Steel, Petroleum Refinery, Petrochemical Units, & Textiles, are expected to follow suit.

Decarbonization has thus ceased to be merely a public relation exercise; it is now a regulatory mandate having financial consequences.

The notification binds the Obligated Entities in a binary outcome based on their performance:

- Beat the Target: Earn Carbon Credit Certificates (CCCs), creating a tradeable bankable asset and adding to profitability.

- Miss the Target: Face a compliance obligation to purchase CCCs, creating a direct liability and hitting profitability.

For emission heavy industries, the cost of carbon will now become a verifiable line item.

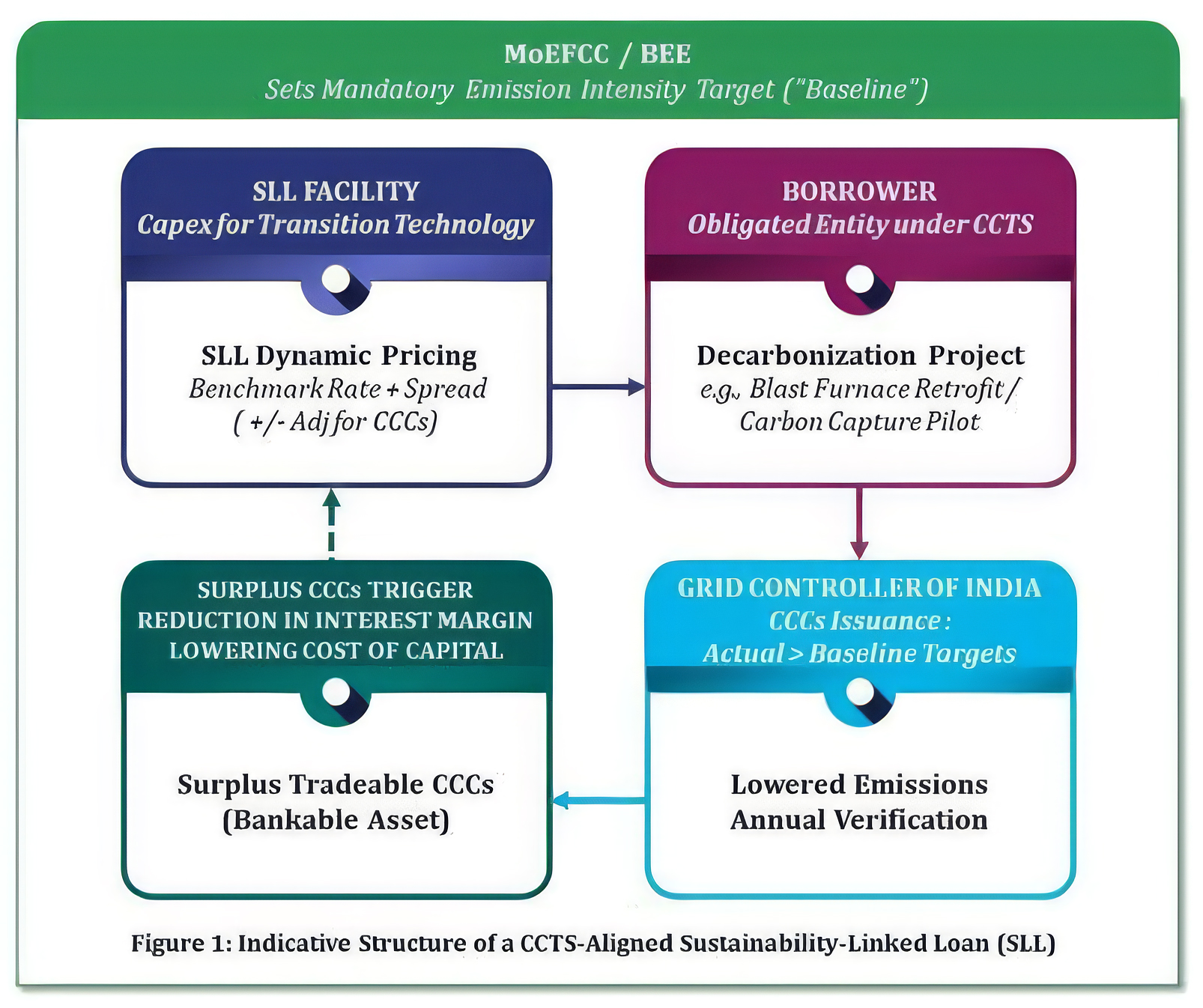

The Structure of Wiring the CCTS into SLLs

Bridging the gap between a company’s current baseline and its mandatory target, the CCTS-aligned SLLs is expected to emerge as a new financing avenue. In this symbiotic structure of SLLs, lenders finance the capex to install necessary technology / systems / infrastructure; the CCTS framework ensures operational rigour and the SLL mechanism provides the pricing incentive to accelerate brown transition. Structurally, it moves beyond standard financing to create a closed-loop system where regulatory compliance directly impacts the cost of capital.

Figure 1 below illustrates the mechanical flow of capital, regulation, and carbon assets in this new deal structure.

As illustrated in Figure 1, the mechanism relies on three interconnected flows:

The Regulatory Anchor

MoEFCC and BEE establish the Compliance Baseline. This significantly mitigates the risk of Ambition Washing—the baseline is non-negotiable. The Grid Controller of India serves as the scheme’s operational backbone by acting as the Carbon Registry. It maintains the central ledger for the Indian Carbon Market, recording issuance, transfer, and surrender/retirement of CCCs to ensure transparency.

The Borrower & The Lender

The Borrower utilizes the SLL provided by lenders specifically for Decarbonization Projects such as blast furnace retrofits, waste heat recovery systems, or carbon capture pilots (technology still being nascent for carbon capture).

Conventional SLLs are typically general corporate purpose facilities, where the borrower uses funds flexibly across operations. However, in the extant case, SLL can be structured as Sustainability-Linked Project Specific Finance (SLPF) facility, which will be utilised for construction of a specific asset. The pricing mechanism is inspired by the dynamic step-down logic of a typical corporate SLL. This allows the borrower to benefit from project-specific tenor and retain the brown transition incentive.

The Feedback Loop

Surplus CCCs generated by the project act as the Key Performance Indicators (KPI). Verification of these credits triggers the interest rate step-down.

Ensuring Transaction Integrity

A CCTS-linked loan is only as robust as its covenants. The diagram above represents the high-level structural details. Accomplishing the transaction depends entirely on the fine print of the term sheet agreed between the parties. There is a risk that lenders may accept loose targets or structural loopholes that render the SLL ineffective; a practice often defined as Greenwashing. To ensure these instruments hold water with both regulators and lenders, some of the structural red flags (detailed in Box 1) and regulatory stack (detailed in Box 2) that deal teams can consider addressing are as under: –

The Value Equation

With the structural integrity secured, the focus shifts to the broader market impact and adoption of SLL products. For lenders, CCTS effectively solves the verification problem, they no longer need to invent targets. Lenders can simply adopt the MoEFCC’s emission trajectory. The regulation thus provides the technical baseline that was previously missing. The credit lines from Development Finance Institutions (DFIs) and Multi-lateral Institutions (MLIs) are also available for transition finance. This provides an opportunity for the Indian lending fraternity to deploy SLL products leveraging the SLL lines from DFIs and MLIs.

For borrowers, it creates three simultaneous value streams that effectively subsidize the cost of capital. Firstly, the financial benefit in terms of the SLL interest discount. Secondly, the commercial benefit arising from revenue from the sale of surplus CCCs. Thirdly, the operational benefit in terms of energy efficiency (e.g., from Waste Heat Recovery).

Key Challenges

Even with robust structures, execution can face friction from key aspects while the structure evolves.

Price Volatility

Price discovery for CCCs remains critical as the market is at the nascent stage. Structuring interest rate based on the monetary value of credits generated may be risky until a stable trading history is established. India’s CCTS targets to incorporate a ‘floor and forbearance price’ mechanism from launch, designed to stabilize prices and prevent early market crashes as evident in European Union (EU) Emission Trading System (ETS). It also draws lessons from Renewable Energy Certificate (REC) market in India where floor and forbearance (caps) were introduced as a regulatory intervention and upon the market maturing floor price has been withdrawn. Till such time the trading of CCCs commence, linking the pricing of such SLLs to the volume of verified credits generated shall be a more prudent approach.

Misalignment of verification and interest reset date

The timeline for Accredited Carbon Verification Agencies to verify emissions, and for the issuance of CCCs through registry may not align perfectly with interest reset dates. Loan documentation may accommodate such lags to handle these administrative delays so that the borrowers continue to avail benefit of SLL.

The CCTS can effectively financialize carbon. The CCTS targets must not be viewed solely as a regulatory burden rather it can be envisioned as an avenue which can assist in lowering the overall finance cost of a borrower. The cost of capital is now inextricably linked to the cost of carbon and therein lies the convergence.

As a financing instrument, the SLLs of the coming decade are not just about signalling virtues to investors; they are about financing the survival kit for the carbon-constrained economy. Beyond the immediate benefits of compliance and cost savings, these instruments strive to bridge the gap between economic ambition and environmental necessity. With the world transitioning towards sustainable mode, the early movers tend to gain advantage. As it is commonly said, the best time to plant the tree was 20 years ago and the next best time is today.